Volume XXV, No. 20 (No. 667)

Friday, March 15, 2024

A Biweekly Electronic Newsletter

As a public service, Hurwitz Fine P.C. is pleased to present its biweekly newsletter, providing summaries of and access to the latest insurance law decisions from the New York and Connecticut appellate courts and Canadian appellate courts. The primary purpose of this newsletter is to provide timely educational information and commentary for our clients and subscribers.

In some jurisdictions, newsletters such as this may be considered Attorney Advertising.

If you know of others who may wish to subscribe to this free publication, or if you wish to discontinue your subscription, please advise Dan D. Kohane at [email protected] or call 716-849-8900.

You will find back issues of Coverage Pointers on the firm website listed above.

Dear Coverage Pointers Subscribers:

An early Happy St. Patrick’s Day. I’ll be celebrating it in Boston, at the PLRB Claims Conference.

Do you have a situation? We love situations. Our goal is that you don’t have any that you cannot handle! So, we provide training for your professional staff. Hey, if you’ve been sharing this with your colleagues, that’s great, but we can save you a bit of work by having them subscribe directly.

This is our Ides of March issue. A number of the stories from a century ago involves the Ides.

New York Coverage Training:

This may be our last time advertising this program, if you’re interested in signing up. We were hoping that we’d have 100 registered; as of this moment, there are 869 registered, with room to 1000. By the time the next issue comes around, I’m quite certain we will be at capacity. So, if you’re interested in our April 5 Zoom New York coverage training, or you know others who may be, contact me now at [email protected]

If you handle New York coverage work, either as a claim professional or as a lawyer, this training is for you. New York coverage protocols differ significantly from those in other states, primarily because of the statutory requirements set forth in Insurance Law §3420(d). When must a coverage letter be sent? Who is required to receive a copy? What happens if you don’t follow the rules?

If you are preparing to write, for example, a reservation of rights letter on a New York loss, like the ones that you write in other jurisdictions – STOP. You may be shooting yourself in the foot, or heart, or wallet. There may be – and often are – dangerous consequences if one fails to send out a timely, properly copied, coverage letter or if it does not contain a high degree of specificity.

If there is a New York accident and an out-of-state policy and you’re feeling comfortable ignoring New York rules – STOP, read and appreciate what our great state may do to you if you fail to follow our rules.

The Zoom presentation will take place at 1:00 PM Eastern Time on Friday, April 5, and should last about 75 minutes. There will be time for Q&A. For claims supervisors reading this message, this is the perfect opportunity for a “lunch and learn”.

Contact me by email to register: [email protected]

Steve Peiper and Dan Kohane are presenting on different topics. We hope to see you there in a couple of days – Please stop by and say hello. We are one of the very few firms in the country where two of our coverage team are presenting programs. Why? Cuz we love what we do to help the insurance industry.

Contractual Indemnity & Additional Insureds Liability

State Approved CE Credits: DE FL NH NC TX

Tuesday, March 19 — 10:30 - 12:00

Wednesday, March 20 — 8:30 - 10:00

John Hanlon, Director of Complex Claims, Kemper Corporation, Charlotte, NC

Dan Kohane, JD, Senior Partner, Hurwitz Fine P.C., Buffalo, NY

-

Distinguish between an insurer's obligations to those who qualify as additional insureds and those who benefit from contractual indemnity obligations.

-

Evaluate how tenders of defense and indemnity should be made under both policy and trade agreement.

-

Describe the protocols to consider when tenders are received under both insurance policy and contracts.

-

Identify the relevant factors when sending or receiving tenders.

CGL Policy & Work Product Coverage Conundrums

State Approved CE Credits: FL NC

Monday, March 18 — 3:30 - 5:00

Wednesday, March 20 — 8:30 - 10:00

Renee Carnuche, CPCU CIC SCLA AIC , VP Field Claims II, Erie Insurance Group, Erie, PA

Steven E. Peiper, JD, Shareholder, Vice President, Hurwitz Fine P.C., Buffalo, NY

-

Explore coverage triggers encountered in work product cases.

-

Identify policy coverage issues including property damage, occurrence, work product exclusion, and exceptions to those exclusions.

- Evaluate work product coverage issues and potentially multiple policies/policy periods triggered.

Need a mediator for an insurance dispute? Coverage mediation is a thing! Subject matter expertise may be useful.

Hey coverage lawyers. Hey professionals. Have you and a friend, adversary, or lawyer for whom who have respect reached a stalemate on a coverage dispute? Look, we know each other. We know that. We don’t want to litigate every coverage disagreement. Why? Because the position we oppose today may be the one we advocate tomorrow. Face it. We all understand that.

Let me help mediate your disagreement to see if there is some mutual agreement we can reach that will not box us into a corner. Reach out to me. I will be pleased to mediate your dispute.

My partners, Mike Perley and Ann Evanko, are also available to help resolve other challenges.

You don’t want adverse precedent that will bite you next time you might have a slightly different view on coverage issues. You don’t want to spend tens of thousands of dollars to litigate a coverage issue before a motion judge or appellate justice that knows as much about insurance coverage as you do about nuclear physics. For those in the Western District of New York, I am certified by the Court and on the WDNY Mediation Panel as are Mike and Ann.

Try mediation.

Newsletters:

We have other firm newsletters to which you can subscribe by simply letting the editor (or me) know, including a new publication, which was created to advise on business and employment law questions:

-

Premises Pointers: This monthly electronic newsletter covers current cases, trends and developments involving premises liability and general litigation. Our attorneys must stay abreast of new cases and trends across New York in both State and Federal Court and will now share their insight and analysis with you. This publication covers a wide range of topics including retail, restaurant and hospitality liability, slip and fall accidents, snow and ice claims, storm in progress, inadequate/negligent security, inadequate maintenance and negligent repair, service contracts, elevator and escalator accidents, swimming pool and recreational accidents, negligent supervision, assumption of risk, tavern owner and dram shop liability, homeowner liability and toxic exposures (just to name a few!). Please drop a note to Jody Briandi at [email protected] to be added to the mailing list.

-

Labor Law Pointers: Hurwitz Fine P.C.’s Labor Law Pointers offers a monthly review and analysis of every New York State Labor Law case decided during the month by the Court of Appeals and all four Departments. This e-mail direct newsletter is published the first Wednesday of each month on four distinct areas – New York Labor Law Sections 240(1), 241(6), 200 and indemnity/risk transfer. Contact Dave Adams at [email protected] to subscribe.

-

Products Liability Pointers: Whether the claim is based on a defective design, flawed manufacturing process, or inadequate instructions/warnings, product liability litigation is constantly evolving. Products Liability Pointers examines recent New York State and Federal cases as well as high court decisions from other jurisdictions, keeping our readers up to date with the latest developments and trends, and providing useful practice tips and litigation strategies. This monthly newsletter covers all areas of product liability litigation, including negligence, strict products liability, breach of warranty claims, medical device litigation, toxic and mass torts, regulatory framework and governmental agencies. Contact V. Christopher Potenza at [email protected] to subscribe.

- Medical & Nursing Home Liability Pointers. Medical & Nursing Home Liability Pointers provides the latest news, developments, and analysis of recent court decisions impacting the medical and long-term care communities. Contact Elizabeth Midgley at [email protected] to subscribe.

Beware the Ides of March – If you Have a Coal Bin – 100 Years Ago:

Lancaster New Era

Lancaster, Pennsylvania

15 March 1924

Peiper on Property (and Potpourri):

A quick note today to invite all of you PLRB attendees to come see Dan and John Hanlon’s risk transfer program. It is a very good investment of time, and you’ll be quite glad that you did.

While you’re there, you can also hang around to catch Renee Carnuche, of Erie Insurance fame and tribute, and your author for a review of the CGL work product exclusions. We’ll keep you entertained, and we won’t interfere with your St. Patrick’s Day festivities.

We review another interesting business interruption claim again this week. The Appellate Division reiterates that for a claim for loss rents there has to be actual physical damage to the building were the loss rents are claimed. This is because, as you’ve heard here before, business interruption insurance is built on the back of property damage coverage. You can’t have one, without the other.

That’s really all we have to say this week. See you in two more.

Steve

Steven E. Peiper

[email protected]

Beware the Ides of March – If You Are Starting to Plant – 100 Years Ago:

The Cincinnati Enquirer

Cincinnati, Ohio

15 March 1924

THE IDES OF MARCH

To my mind almost the most thrilling time of the whole year is the fifteenth of March-that season so ominously mentioned in Shakespeare, I don’t not “beware the ides of March”- I welcome them! For this is the time when I make the first move towards my flower garden. The blood-curdle that used to shudder through m in my schoolgirl days at the sound of those awful words has changed now to a little inward gurgle of joy, for at last I may plant my seeds in the window boxes and within three days see the first sprouting of the plants that will fill my garden with color all summer through.

I hope that you ordered your seeds when I wrote reminding you of it on the last day of February. It generally takes two weeks or so to get seed orders filled, and while, of course, it will not be too late if you wait until April – or even until the time when you can plant the seeds in the open ground – still, the earlier you start, the better success you will have, as transplanted seedlings are much stronger and sturdier than those which are merely planted outdoors and thinned out.

Barnas on Bad Faith:

Hello again:

Just a short note from me this week as I am in Chicago for DRI. I am looking forward to presenting on business risk exclusions on Friday morning. If you are here, I hope you are able to stick around for that and that you will come say hello. I have first party cases in my column this week where courts in Oklahoma and Texas dismissed good faith and fair dealing claims arising from alleged hail damage. The moral of the story is a familiar one: a good faith dispute as to insurance coverage does not equate to bad faith.

Brian

Brian D. Barnas

[email protected]

Beware the Ides of March – Keep Your Snow Gear Handy – 100 Years Ago:

Birmingham Post-Herald

Birmingham, Alabama

15 March 1924

GROUND HOG DAYS GONE

Ides of March Brings Snow in Reform

REFORM, Ala., March 14. – (special.) – The Ides of March were ushered in today, accompanied by one of the heaviest snow falls in the history of this part of Pickens county. The snow and a hominy rain began falling Thursday about 9 o’clock, and by 12 the ground was covered and by night fall the covering was over six inches deep. The temperature was not very low and there was not the slightest breeze stirring.

The worst damage done is due to the fact that most people had burned up their winter’s coal pile, and not contemplating a heavy snow this late in the season, were caught without much fuel on hand. This winds up the sixth week since the ground hog came forth on February 2 and seeing his shadow returned for the final installment of winter.

Lee’s Connecticut Chronicles:

Dear Nutmeg Newsies:

Back home again in Connecticut, at least long enough to do some laundry. Just returned from a work/family trip to Tampa Bay where I spent some quality time with a client. In this era of Zoom, Teams, and Webex, which have made life immensely easier, nothing compares to sitting in the same room, face-to-face with another person to build connection. Next week, it’s off to Los Angeles and Palm Springs for another family/work trip and some mid-century modern architecture in the desert.

Until then, keep keeping safe.

Lee

Lee S. Siegel

[email protected]

Beware the Ides of March – Origin – 100 Years Ago:

The Evening Journal

Wilmington, Delaware

15 March 1924

How it Started

BY JEAN NEWTON

“The Ides” are a division of the ancient Roman calendar and were the 15th of March, May, July and October. The other month, “The Ides” was the 13th.

The expression “The Ides of March” has come to mean the portending of an ominous date. It was first used in Shakespeare’s dram Julious Caeser, where the soothsayers warned the conqueror of Gaul to “Beware the Ides of March.” Caeser scorned the warning and on the morning of the “Ides of March” he taunted them, saying:

“The Ides of March are Come.”

“Aye, Caeser, but not gone,” they answered.

Before the “Ides” were passed Caeser had been slain.

Kyle's Noteworthy No-Fault:

Dear readers,

In this week’s No-Fault case, the insurer brough an action seeking a de novo review of the insured’s No-Fault claims sought in this case pursuant to Insurance Law Section 5016(c). Prior to this action, an arbitrator issued an award to the medical provider for services rendered to the insured after the insurer denied coverage on the basis that the medical treatment was not necessary and not casually related to the accident. The medical provider than brought the motion before the court in this case seeking to compel the insurer to furnish all information pertaining to any other arbitration with any medical provider regarding the injuries sustained by the insured in the subject accident. The court ultimately granted the motion, to produce the entire claims file, holding that the information sought was highly relevant and material and necessary, subject to a protective order to protect sensitive information in the file.

Until next time,

Kyle

Kyle A. Ruffner

[email protected]

Beware the Ides of March – Loan Payments Due – 100 Years Ago:

The Ashville Times

Asheville, North Carolina

15 March 1924

Ryan’s Federal Reporter:

Hello Loyal Coverage Pointers Subscribers:

Although my own ESPN+ broadcasting season for Niagara University Women’s Basketball has come to a close, the work is not done. The Purple Eagles were triumphant in their MAAC Championship quarter-final matchup against Quinnipiac yesterday afternoon and will square off tomorrow against today’s winner between Siena and Mount St. Mary’s. Of note, #25 ranked Fairfield had a bit of a scare against Rider in their quarter-final matchup, but ultimately pulled away and prevailed. Fairfield will take on today’s winner between Manhattan and Canisius. There is nothing quite like March Madness.

This St. Patrick’s Day weekend, I had an interesting opportunity fall into my lap, so we’ll appropriately call it the luck of the Irish. I will be calling play-by-play for two New York State Hockey Championship semifinal games from Dwyer Arena on Sunday morning. The full slate of games can be found here, and while I do not know the teams, my assignments include NYSAHA Tier II 14U Semi 1 and Tier I 16U Semi 1. Nothing like new opportunities to rekindle a growth mindset once again. Now, does anyone know how to play hockey?

This edition, my column contains a write-up for a district court decision involving a request for the deposition of coverage counsel. I’ll leave it there and you’ll have to read on.

Until next time,

Ryan

Ryan P. Maxwell

[email protected]

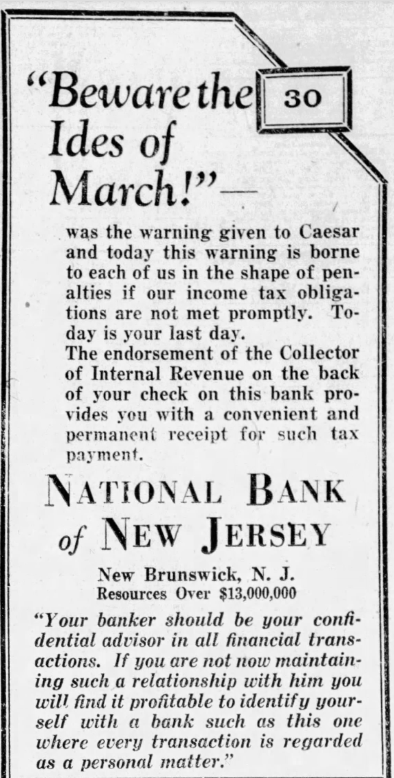

Beware the Ides of March – It’s Income Tax Day – 100 Years Ago:

The Salt Lake Tribune

Salt Lake City, Utah

15 Mar 1924

Editor’s Note – When the Income Tax was first enacted, in 1913, taxes were due on March 1. Three years later, that changed to March 15. In 1955, in order to take the pressure off of IRS employees, the due date for tax returns was moved to April 15.

Storm’s SIU:

Hi Team:

As I write this I am flying back to Buffalo from an awesome week in Key West. More interesting cases next edition. For this edition I’ll just sing…

Off the Florida Keys

There's a place called Kokomo

That's where you wanna go

To get away from it all

Bodies in the sand

Tropical drink melting in your hand

We'll be falling in love

To the rhythm of a steel drum band

Down in Kokomo

Aruba, Jamaica, ooh, I wanna take you to

Bermuda, Bahama, come on pretty mama

Key Largo, Montego

Baby, why don't we go? (Ooh, I wanna take you down to Kokomo)

We'll get there fast

And then we'll take it slow

That's where we wanna go

Way down in Kokomo…

Have a great two weeks,

Scott

Scott D. Storm

[email protected]

Beware the Ides of March – Banks Used Same Ad Around the Country – 100 Years Ago:

The Central New Jersey Home News

New Brunswick, New Jersey

15 Mar 1924

Fleming’s Finest:

Hi Coverage Pointers Subscribers:

Now that it is finally light outside again in the evening, I hope you are able to get outside and enjoy the extra daylight. In this week’s case, the Colorado Supreme Court extended the notice-prejudice rule to occurrence-based, first-party homeowners’ property insurance claims.

Until next time,

Kate

Katherine A. Fleming

[email protected]

Beware the Ides of March – So, Buy Insurance – 100 Years Ago:

The Daily Sentinel-Tribune

Bowling Green, Ohio

15 Mar 1924

Gestwick’s Garden State Gazette:

Dear Readers:

Much like the Roman Senate did on the Ides of March, I, too, must take a recess, as I am travelling on business this time around. “Et tu, Brute?” you may ask. My response would be, “yeah, me too,” although I doubt that’s actually how Brutus responded to Caesar. See you in two weeks. Until then, carpe diem.

Evan

Evan D. Gestwick

[email protected]

“Pay Money or Die” – He Didn’t and Remained Alive– 100 Years Ago:

The Buffalo News

Buffalo, New York

15 Mar 1924

MUST PAY $2000 OR DIE,

JAMESTOWN MAN TOLD

Deputy Sheriffs Investigate “Black Hand” Plot Without Success

JAMESTOWN, March 15. – Philip Lombardo of this city received a Black Hand letter in the mail yesterday, directing him to save his life by leaving $2000 at midnight under the Main Street bridge in West field. Deputy Sheriffs were sent to watch the spot when Lombardo reported the threat to the authorities, but no one showed up to get the money.

O’Shea Rides the Circuits:

Hey Readers,

Last week my Newfoundland puppy had his one-year checkup, and I unsettlingly report that he is 150 lbs. Our four-year-old Newfie is only around 110 lbs., so the tables have vastly turned in less than a year and a half. In other news, the weather is turning in favor of Spring. With this turn yardwork begins, especially when you omitted to rake leaves in the fall . . .

This week I have a couple of cases. The first deals with an insured contesting an appraisal award, based upon the evidence the umpire reviewed to determine the actual cash value of the loss. The second concerns federal procedure, specifically what constitutes a final judgment. In the second case, the court considered whether issue resolution could qualify as claim adjudication.

Ryan

Ryan P. O’Shea

[email protected]

Here’s a First – Using Radio Broadcasts to Encourage Voter Registration – 100 Years Ago:

The Buffalo News

Buffalo, New York

15 Mar 1924

USE RADIO TO URGE

VOTERS TO REGISTER

Special to the Buffalo Evening News

CHICAGO, March 15. – For the first time in the history of Chicago and Cook county radio is being used in connection with the registration of voters next Tuesday. County Judge Jarecki has arranged with the operators of a broadcasting station here to co-operate with the election board in bringing the voters out for registration.

Beginning today the message was sent over the radio to thousands of listeners urging them not to become “civic slackers,” but to go to the polls and register. The message will be sent out as often as the broadcasting station finds it convenient to do so.

Louttit’s Legislative and Regulatory Roundup:

Nothing to report at this time. See you in two weeks.

Rob

Robert P. Louttit

[email protected]

Movies by Radio Predicted – 100 Years Ago:

The Buffalo News

Buffalo, New York

15 Mar 1924

MOVIES BY

RADIO SOON

HE PREDICTS

C. Francis Jenkins, Washington Inventor, Asks Modification of Bill to Permit Transmission of Pictures Through Air.

Special to the Buffalo Evening News

WASHINGTON, March 15. – “Movies by radio in your own home,” was predicted as an early development in testimony yesterday before the house merchant marine and fisheries committee by Francis Jenkins, inventor, of this city. He asked for a modification of the White radio bill to prevent any regulation that might interfere with the transmission of pictures.

The committee ended hearings yesterday morning. The measure will be referred to a subcommittee and whipped into final shape for reporting to the house. Mr. Jenkins said he and his associates expect to establish soon a broadcasting station for transmitting photographs through the air. Mr. Jenkins said that pictures had already been sent from Washington to Philadelphia under a new method.

He prophesied people soon would be able to witness in their own homes big league baseball games through an attachment on their radio sets, and also see performers on distant stages. These transmissions will be instantaneous with the music and singing or whatever the performance may be, according to Mr. Jenkins.

Rob Reaches the Threshold:

Hello Readers,

At the time of our last publication, I asked for the good vibes, weather wise, to keep carrying on. I appreciate Mother Nature for acknowledging my request – because we continue to enjoy mostly record highs in the Western New York area. I say ‘mostly’ because we did have one snow day this past Sunday, which just happened to be my birthday. This is the price I had to pay for sunshine and golf in early March.

For this installment, we jump back to the First Department and examine a Decision which analyzes the evidence submitted in motion for summary practice by both sides. Here, the court found numerous issues with plaintiff’s opposition.

I hope you all enjoy the read.

Rob

Robert J. Caggiano

[email protected]

The Value of Love – 100 Years Ago:

The Brooklyn Daily Eagle

Brooklyn, New York

15 Mar 1924

BLACK TO APPEAL

$46,000 LOVE-BALM

VERDICT FOR BABB

Flatbush Manufacturer Claims

“Platonic Friendship” Award Is Ridiculous.

Clyde E. Black, president of the Black Knitting Mills Company, whose “platonic friendship” with Mrs. Charles Babb, pretty 24-year-old model, was valued at $46,000 by a jury yesterday, declared today that the verdict was “ridiculous” and said he intends to appeal the case. Black was sued in the Supreme Court in Queens by Charles Babb of 353 Linden Ave., Flatbush, husband of the model. Mrs. Babb, adding her protestation to that of her friend who must part with a goodly portion of his wealth, declares Babb is not “worth $46,000 of anyone’s affection.

Mrs. Babb was the only witness called yesterday. She admitted going to Bermuda with Black and that on the return trip they occupied the same cabin. There was nothing between them, though, she said but “platonic friendship.” “Apple sauce,” one of the Jurors called this testimony when the verdict was in.

Goldberg’s Golden Nuggets:

Hello Readers,

Another two weeks in the books but an hour of sleep left behind. This week I bring to you a rear-end collision that is backwards to how we typically see rear-end collisions play out. I also highlight a case out of the Third Department, originating at the Workers’ Compensation Board, which gives us a good review of what is convenient and reasonable when designating the location of an IME, that has applications outside of the often-isolated realm of the Workers’ Compensation Board.

Enjoy!

Josh

Joshua M. Goldberg

[email protected]

Can you A-Ford It? – 100 Years Ago:

The Farmingdale Post

Farmingdale, New York

15 Mar 1924

LaBarbera’s Lower Court Library:

Hello Readers!

This past weekend I got two snails for my aquarium. This means my count is up to four fish, two frogs, and two snails. Although I set up this tank three months ago, I think it may already be time for an upgrade. For those of you who have never dabbled, I highly recommend it. It is embarrassing to admit how long I can spend watching everything swim around.

For this week, I have a first-party insurance coverage dispute litigated in New York County. Ultimately, the court granted the insurer’s motion for summary judgment, and found that the insured’s claims were time barred under the suit limitation provision contained within the policy, which required any lawsuit be brought against the insured within two years of the direct physical loss or damage. However, the court also decided that the late notice disclaimer by the insurer could not be sustained under Insurance Law § 3420[c][2][C]. Unsurprisingly, the insurer has filed a limited motion to reargue, highlighting the fact that Insurance Law § 3420 does not apply to first-party property insurance claims.

Isabelle

Isabelle H. LaBarbera

[email protected]

Shocking! – 100 Years Ago:

The Ithaca Journal

Ithaca, New York

15 Mar 1924

North of the Border:

I’m on the road again this week – this time in Chicago, in my capacity as President of Canadian Defence Lawyers, attending a DRI Regional Meeting that is being held concurrently with DRI’s 2024 DRI Insurance Coverage and Claims Institute. I am catching up with old friends and making new ones.

My column this week discusses a case of an insurer who continued to engage with its insured following the expiration of the limitation period. Can the claim proceed despite the insured’s failure to file within the limitation? Is the insurer estopped? What do you think?

Heather

Heather A. Sanderson

Sanderson Law, Calgary, Alberta

[email protected]

Headlines from this week’s issue, attached:

KOHANE’S COVERAGE CORNER

Dan D. Kohane

[email protected]

- A Failure to Prove that Required Excess Coverage was Procured, Means a “Failure to Procure” Claim Should Not be Dismissed. Without a Grave Injury, a Common Law Claim against the Plaintiff’s Employer Cannot be Maintained

- No Coverage for Employee Injuries. No Waiver of Defenses Under Insurance Law Section 3420(d)(2)

- Neither Prior Publication Exclusion Nor Criminal Acts Exclusion Bars Defense Obligation under Policy. Extrinsic Evidence Does Not Clarify Ambiguities in Complaint

PEIPER on PROPERTY (and POTPOURRI)

Steven E. Peiper

[email protected]

- Business Interruption Claim Based on Lost Rents Must Still Show Physical Damage to the Insured Structure

- Mere Inconvenience of Witnesses is Insufficient to Support Change of Venue Motion

BARNAS on BAD FAITH

Brian D. Barnas

[email protected]

- Good Faith and Fair Dealing Claim Dismissed Based on Reasonable Dispute of Coverage Under Policy

- Good Faith and Fair Dealing Claim Dismissed Based On Reasonable Dispute Regarding Coverage under Policy

LEE’S CONNECTICUT CHRONICLES

Lee S. Siegel

[email protected]

-

Bad Faith Cause of Action Dismissed

-

Simulated Sex Act Not An Occurrence

KYLE'S NOTEWORTHY NO-FAULT

Kyle A. Ruffner

[email protected]

- In Insurer’s Action for De Novo Review of No-Fault Claims, Court Grants Medical Provider’s Motion to Compel Disclosure of All other Arbitrations Between the Insurer and Other Medical Providers for the Insured’s Injuries

RYAN’S FEDERAL REPORTER

Ryan P. Maxwell

[email protected]

- Insurer Successfully Combats Attempt to Depose Coverage Counsel Who Had Ghostwritten Reservations of Rights Letters

STORM’S SIU

Scott D. Storm

[email protected]

- Flying back from vacation in Key West.

FLEMING’S FINEST

Katherine A. Fleming

[email protected]

- Notice-Prejudice Rule Applies to Occurrence-Based First-Party Homeowners’ Property Insurance Claims

GESTWICK’S GARDEN STATE GAZETTE

Evan D. Gestwick

[email protected]

- On the road this edition

O’SHEA RIDES the CIRCUITS

Ryan P. O’Shea

[email protected]

- Insured Cannot Avoid Appraisal Award Based on Argument that Lack of Policy Definition of Actual Cash Value Barred Application of Broad Evidence Rule

- Resolution of Issue Did Not Judicially Resolve Crossclaim Barring Court from Hearing Appeal Due to Lack of Final Judgment

LOUTTIT’S LEGISLATIVE and REGULATORY ROUNDUP

Robert P. Louttit

[email protected]

- Nothing to Report at this time

ROB REACHES the THRESHOLD

Robert J. Caggiano

[email protected]

- First Department Unanimously Affirmed, Without Costs, a Decision Granting Summary Judgment in Favor of Defendant Where Plaintiff’s Evidence Failed to Raise an Issue of Fact on Whether He Suffered Serious Injury Within the Meaning of Insurance Law § 5102(d)

GOLDBERG’S GOLDEN NUGGETS

Joshua M. Goldberg

[email protected]

- Defendant Rear Ended by Plaintiff Loses Motion for Summary Judgment

- Reasonableness of IME Location

LABARBERA’S LOWER COURT LIBRARY

Isabelle H. LaBarbera

[email protected]

- Insured’s Declaratory Judgment Action Dismissed On Summary Judgment Pursuant to the Suit Limitation Clause in Policy

NORTH of the BORDER

Heather A. Sanderson

Sanderson Law, Calgary, Alberta

[email protected]

- An Insurer that has Notified its Insured of a Pending Litigation Will Not be Estopped from Relying upon that Limitation once it Expires, even if it Requests Additional Information about the Claim Following the Expiration, unless there is a Clear Admission of Liability to Pay the Claims in Dispute, or Extends a Clear Promise Not to Rely upon the Limitation

That’s all there is and there is no more. See you in Boston or two weeks from now, right here.

Dan

Hurwitz Fine P.C. is a full-service law firm providing legal services throughout the State of New York and providing insurance coverage advice and counsel in Connecticut.

In addition, Dan D. Kohane is a Foreign Legal Consultant, Permit No. 000241, issued by the Law Society of Upper Canada, and authorized to provide legal advice in the Province of Ontario on matters of New York State and federal law.

NEWSLETTER EDITOR

Dan D. Kohane

[email protected]

ASSOCIATE EDITOR

Agnes A. Wilewicz

[email protected]

COPY EDITOR

Evan D. Gestwick

[email protected]

INSURANCE COVERAGE/EXTRA CONTRACTUAL LIABILITY TEAM

Dan D. Kohane, Chair

[email protected]

Steven E. Peiper, Co-Chair

[email protected]

Michael F. Perley

Agnieszka A. Wilewicz

Lee S. Siegel

Brian F. Mark

Scott D. Storm

Brian D. Barnas

Robert P. Louttit

Ryan P. Maxwell

Joshua M. Goldberg

Kyle A. Ruffner

Katherine A. Fleming

Evan D. Gestwick

Ryan P. O’Shea

Isabelle H. LaBarbera

FIRE, FIRST PARTY AND SUBROGATION TEAM

Steven E. Peiper, Team Leader

[email protected]

Michael F. Perley

Scott D. Storm

Brian D. Barnas

NO-FAULT/UM/SUM TEAM

Dan D. Kohane

[email protected]

Alice A. Trueman

Joshua M. Goldberg

APPELLATE TEAM

Jody E. Briandi, Team Leader

[email protected]

Topical Index

Peiper on Property and Potpourri

Barnas on Bad Faith

Ryan’s Federal Reporter

Gestwick’s Garden State Gazette

Louttit’s Legislative and Regulatory Roundup

Rob Reaches the Threshold

LaBarbera’s Lower Court Library

KOHANE’S COVERAGE CORNER

Dan D. Kohane

[email protected]

03/14/24 Douglas v. Roseland Development Associates, LLC

Appellate Division, First Department

A Failure to Prove that Required Excess Coverage was Procured, Means a “Failure to Procure” Claim Should Not be Dismissed. Without a Grave Injury, a Common Law Claim against the Plaintiff’s Employer Cannot be Maintained.

DFC and DiFama's moved for summary judgment seeking to dismiss Roseland’s claim for breach of contract for failure to procure insurance. DFC and DiFama failed to establish, as a matter of law, that they procured liability insurance with a $10,000,000 per-occurrence limit as DFC was contractually obligated to purchase.

Additionally, while they procured a primary policy which named defendants as additional insureds, they failed to show that they procured an excess liability policy naming defendants as additional insureds, as required by the contract.

However, the defendants' third-party claims for common-law indemnification and contribution asserted against DiFama should have been dismissed. Under Workers' Compensation Law § 11, with a grave injury, a common claim for contribution or indemnity cannot be maintained against the injured plaintiff’s admitted employe.

The issue of fact as to whether DFC is the alter ego of DiFama does not preclude granting summary judgment to DiFama. DFC is not seeking an extension of Workers' Compensation Law § 11 to itself.

03/12/24 823 Second Avenue v. Utica First Insurance Company

Appellate Division, First Department

No Coverage for Employee Injuries. No Waiver of Defenses Under Insurance Law Section 3420(d)(2)

Although 823 Second Avenue qualifies as an insured under the policy issued to its tenant, P.R. Crepe, Ltd, there was an operative exclusion that removed coverage, an employee exclusion. There was an “incidental contract” exception to the exclusion, but it was up to 823 Second to establish that there was an “incidental contract” involved, and the insured failed to do so. The court does not discuss what may be, or may not be, an “incidental contract” but to read the arguments that convinced the court this was not an “incidental contract”, click here.. The court noted that:

It was claimed that Utica waived its right to disclaim coverage under Insurance Law §3420(d)(2). Utica sent two disclaimer letters to plaintiff on consecutive days. Although the second letter indicated that Utica was disclaimer coverage to its named insured, P.R. Crepe,823 knew from the first letter that it was also being denied coverage. The court noted:

The statute 3420(d)(2) is not intended to be a technical trap that would allow interested parties to obtain more than the coverage contracted for under the policy",

03/05/24 Wesco Insurance Company v. Nunez Dental Services, P.C.

Appellate Division, First Department

Neither Prior Publication Exclusion Nor Criminal Acts Exclusion Bars Defense Obligation under Policy. Extrinsic Evidence Does Not Clarify Ambiguities in Complaint

Wesco failed to establish, as a matter of law, that they had no duty to defend Nunez in the underlying action. It failed to meet their burden of establishing that they have no duty to defend on the basis that a prior publication exclusion bars coverage, as the underlying complaint does not indicate that the injury arose out of any publication which first took place before the beginning of the policy periods. The extrinsic evidence plaintiffs rely on, which was obtained in this subsequent litigation, and which does not serve to clarify any alleged ambiguities in the underlying complaint, does not relieve them of their duty to defend Nunez.

Plaintiffs have also not established, as a matter of law, that the prior publication exclusion precludes indemnification.

The record establishes that an image of the plaintiff in the underlying action was first used in 2009, but the record does not establish what that use consisted of. It cannot be determined on this record that the publications attached to the underlying complaint, which were retrieved in approximately late 2018, consisted of substantially the same offending material as was published in 2009.

Moreover, the plaintiff in the underlying action alleged that her images had been altered in order to make it appear that she was a customer of or endorsed Nunez's dental practice, and the record does not establish whether the 2009 publication was also so altered. Without the 2009 publication in the record, the court found find that defendants have not established, as a matter of law, that the prior publication exclusion is inapplicable.

The court also found that the criminal acts exclusion did not bar coverage in this case. The exclusion at issue applies to injury arising out of a criminal act committed by Nunez or at the direction of Nunez. The record does not establish that Nunez has been convicted of any crime related to the events addressed in the underlying complaint nor does it even show that Nunez was ever charged with a crime). Multiple issues of fact exist concerning Nunez's knowledge of whether Nunez had obtained the rights to use plaintiff's image, whether Nunez acted with the required mens rea to constitute a misdemeanor under Civil Rights Law § 50, and whether it was a separate party, namely, an individual hired to advertise Nunez's business, who committed the alleged criminal act without being directed to do so by Nunez. While it is possible that the alleged conduct may be found to constitute a misdemeanor, we note that this is not a case were Nunez was convicted of anything, or where Nunez has failed to propose a scenario in which Nunez's conduct was tortious yet not criminal.

PEIPER on PROPERTY (and POTPOURRI)

Steven E. Peiper

[email protected]

Property

03/14/24 87 Uptown Road, LLC v. Country Mut. Ins. Co.

Appellate Division, Third Department

Business Interruption Claim Based on Lost Rents Must Still Show Physical Damage to the Insured Structure

Plaintiff owned/operated a complex with 11 apartment buildings providing student housing in Ithaca, New York. In October of 2019, a fire severely damaged Building D of the complex which displaced all tenants residing therein. The subsequent insurance claim sought recovery of damages sustained to the building, but also business interruption losses related to the loss of tenancy at Building D. Plaintiff also sought alleged business interruption losses related to the other buildings at the complex on the theory that the site was less desirable due to the construction and rehabilitation of Building D.

Countrywide rejected the claims for related business interruption, and this lawsuit ensued.

In affirming the denial for tangential business interruption claims, the Court noted that the policy required that any loss be directly tied to the suspension of operations at the damaged building. Here, the other buildings at the complex did not sustain direct physical loss, or at least not enough loss to result in the suspension of business activities thereat.

Plaintiff countered that coverage should still be triggered where, as they alleged, there was a partial suspension or slowdown in occupancy at other buildings. While the Court recognized this nuance in the policy language, it nevertheless returned to the fact that there was no discernible property damage which constituted a “material alteration or a complete and persistent dispossession of the insured property.” As such, all compensable damage was limited to Building D.

Potpourri

03/14/24 Corner of Walnut, LLC v. Tompkins Ins. Agencies, Inc.

Appellate Division, First Department

Mere Inconvenience of Witnesses is Insufficient to Support Change of Venue Motion

Plaintiff engaged Tompkins to serve as its insurance broker for a project in Batavia, New York. During renovations of buildings at the project, one particular structure collapsed. Plaintiff’s insurer denied the claim based on an exclusion for a “standing building or structure.”

Plaintiff, however, allegedly requested that Tompkins specifically ensure it would have coverage for the existing buildings at the jobsite. As such, the instant lawsuit was commenced in and for New York County Supreme Court.

Tompkins moved to change venue, presumably to an upstate location. In reversing the trial court, the Appellate Division noted that Tompkins did not meet its burden because the bald statements it introduced that suggest non-party witnesses will be inconvenienced by the selected venue is an insufficient reason to alter an otherwise appropriately selected venue. Further, even though the witnesses may be inconvenienced, the collapse of the building is not really germane to the operative question of whether Tompkins failed to place proper coverage. Under these circumstances, the witnesses to coverage placed in New York City are not inconvenienced by the selected venue.

BARNAS on BAD FAITH

Brian D. Barnas

[email protected]

03/07/24 McKenzie v. Hanover Insurance Company

United States District Court, Eastern District of Oklahoma

Good Faith and Fair Dealing Claim Dismissed Based on Reasonable Dispute of Coverage Under Policy

Plaintiffs obtained a homeowners insurance policy from Hanover that had a one percent deductible for wind and/or hail claims. Plaintiffs submitted a claim for roof damage caused by wind and hail. Two days later, an investigator inspected the property and submitted a report. The report found no evidence of hail damage. However, there was damage to the roof’s metal accessories and granule loss and deterioration on roof shingles.

Defendant reviewed the report and concluded there was no hail damage. It concluded the damage was due to defective shingles and that the covered damage to the metal accessories was below the deductible. The claim was denied. After Plaintiffs hired a roofing contractor to dispute the denial, Defendant retained a licensed engineer. The engineer concluded there was no evidence of hail damage but there was age related deterioration to the roof. The claim was denied again.

Plaintiffs filed a lawsuit alleging breach of contract and breach of the duty of good faith and fair dealing. Defendant moved for summary judgment on the bad faith claim. Plaintiffs argued that Defendant failed to conduct an adequate investigation and promptly pay the claim, but the evidence showed the Defendant immediately investigated. Plaintiffs could not identify what material evidence Defendant overlooked in evaluating the claim. Multiple people inspected the property, and there was a disagreement on the extent of damages and coverage. A legitimate dispute concerning coverage is not bad faith. The court also rejected Plaintiffs argument that Defendant misconstrued the policy by finding that the damage was due to causes other than hail based upon the clear dispute on coverage reasoning.

03/06/24 Nieto v. State Farm

United States District Court, Southern District of Texas

Good Faith and Fair Dealing Claim Dismissed Based On Reasonable Dispute Regarding Coverage under Policy

Nieto had a homeowner’s insurance policy with State Farm covering his home in Brownsville, Texas. The policy had a $3,386 deductible. Nieto filed a claim with State Farm for roof damage caused by a rainstorm. State Farm’s inspector found no accidental direct physical damage to the roof but did find some rot, wear, and tear. Covered damages totaled less than the deductible.

After the insured filed the lawsuit against State Farm alleging breach of contract and breach of the implied covenant of good faith and fair dealing, State Farm sent two experts to the property. Both experts opined that there was no storm damage and that any damage arose from wear and tear, improper installation of solar panels, and construction defects.

State Farm moved for partial summary judgment dismissing the good faith and fair dealing claim. The court granted the motion because the evidence showed nothing more than a bona fide coverage dispute as to whether the storm or other factors caused the damage to Nieto’s roof. There was no evidence suggesting State Farm acted unreasonably by relying on its adjuster and its experts.

The court also concluded there was no evidence State Farm engaged in common law fraud or misrepresentation. State Farm disputing whether the claim was covered did not amount to fraud or negligent misrepresentation. Plaintiff’s claims pursuant to Texas Insurance Code Section 441.060 was also dismissed because State Farm provided a prompt and reasonable explanation for its denial.

LEE’S CONNECTICUT CHRONICLES

Lee S. Siegel

[email protected]

03/06/24 Vanguard Medical, LLC v. Acrisure, LLC

Superior Court of Connecticut, Waterbury District

Bad Faith Cause of Action Dismissed

In an action against an insurance broker involving claims of failure to procure insurance, breach of fiduciary duty and bad faith, the court granted the broker’s motion to dismiss the bad faith cause of action. The court, as many before it, noted the continuing divergence in pleading standards imposed by Connecticut trial courts.

[t]here is a split of authority among Superior Courts as to what factual allegations are sufficient to constitute the element of bad faith. The first line of cases requires specific allegations establishing a dishonest purpose or malice. The second line of cases generally holds parties to a less stringent standard requiring that a plaintiff need only allege sufficient facts or allegations from which a reasonable inference of sinister motive can be made .... (internal citations omitted).

Ultimately, the court held that under either pleading standard that the plaintiff’s bad faith cause of action failed, as there are no allegations in the amended complaint of sinister motive or dishonest purpose, nor allegations from which the court could infer that such motive existed.

03/06/24 Century-National Ins. Co. v. Belmont

Superior Court of Connecticut, New London District

Simulated Sex Act Not An Occurrence

Granting Century-National summary judgment, the court found that it had no duty to defend the insured who was alleged to have distressed the plaintiff by committing simulated sex acts in her presence.

Belmont was a football player at Bacon Academy, a public high school in Colchester. While he was on the team bus with Brianna Hurlock, a cheerleader, Belmont encouraged a teammate, Jonathan Torres, to perform a simulated act of sexual intercourse by placing his hands on his helmet and thrusting his hips into the helmet. Belmont recorded this and shared the video. Belmont also made sexually explicit comments on the bus ride. Hurlock sued, claiming that Belmont negligently inflicted emotional distress, causing a cascade of damages.

Century-National brought this action seeking a declaration that it did not owe Belmont a defense under his parents HO policy. The carrier argued that the conduct alleged does not amount to an occurrence, that the plaintiff suffered no bodily injury, that the expected or intended injury exclusion and/or the sexual molestation exclusion apply.

The court agreed that, under Connecticut law, emotional injuries that are not preceded by physical injuries do not meet the definition of “bodily injury” under an insurance policy. As a result, since the complaint did not seek damages arising from bodily injury, there was no duty to defend or indemnify. Moreover, the court agreed that the alleged acts were not accidental and therefore not an occurrence and excluded by the expected or intended provision. “Moreover, although courts have “sometimes treated the analyses of whether an act constitutes an ‘occurrence,’ defined as an ‘accident,’ and whether the act falls within the intentional act exclusion separately ... the ultimate inquiry—whether the act was intentional—is the same.”

As an aside, the court denied that the sexual molestation exclusion applied. “There are no allegations in the underlying complaint that Belmont engaged in sexual molestation, corporal punishment or physical or mental abuse of Brianna Hurlock.”

KYLE’S NOTEWORTHY NO-FAULT

Kyle A. Ruffner

[email protected]

02/27/24 American Transit Ins. Co. v. Passaic Orthopedic Group

Supreme Court, Kings County

In Insurer’s Action for De Novo Review of No-Fault Claims, Court Grants Medical Provider’s Motion to Compel Disclosure of All other Arbitrations Between the Insurer and Other Medical Providers for the Insured’s Injuries.

American Transit’s insured was involved in an automobile accident and sought treatment in connection with injuries sustained with multiple medical providers, including the defendant Passaic Orthopedic Group pursuant to the no-fault provisions of the insurance policy. The insurer refused to pay any bills submitted by the provider on the basis that such treatment was not necessary or casually related to the accident. The parties appeared for arbitration and the provider was awarded $9,694.76, which was sustained by a Master arbitrator. The plaintiff insurer commenced this action seeking de novo review of the no-fault claims pursuant to Insurance Law § 5016(c). The provider sought all arbitration information related to other arbitrations between the insurer and other medical providers for the insured’s injuries, and the insurer objected on the basis that the information was not relevant to the defense of this action. The defendant then brought the motion at issue in this case seeking to compel the insurer to furnish all information pertaining to any other arbitration with any medical provider regarding the injuries sustained by the insured.

The court explained that Insurance Law § 5016(c) provides that where an arbitrator's award exceeds $5,000 the insurer or the claimant may institute an action seeking de novo review to adjudicate the dispute. Thus, if the monetary threshold is satisfied then "the entire dispute is subject to a plenary judicial adjudication. Thus, a de novo review, by its very nature, is not a review of the arbitration proceeding itself or the arbitration award but a review of the underlying dispute, as if an arbitration proceeding never occurred, thus contemplating a full adjudication, on the merits, of the parties claims.

In support of its defense, which seeks dismissal of this action and would then confirm the awards of the arbitrators, the medical provider sought the file consisting of all information regarding any arbitrations between the insurer and any medical providers concerning the subject accident. It is well settled that when a party affirmatively places their medical condition in controversy through allegations that an underlying accident cause injury, then prior medical treatment is generally discoverable. While this case involved slightly difference circumstances, where the insurer seeks a review that the injury party suffered no injury and no payments need to be made, the court applied the same reasoning and determined that any information that could rebut or challenge that contention is discoverable. The court emphasized the importance of full and liberal disclosure of any facts bearing on the controversy at issue and that the reach of discovery should be commensurate with the breadth of the plaintiff’s allegations.

In this case, the insurer sought a fresh determination whether the underlying plaintiff, the insured, in fact sustained any injuries and may be entitled to no-fault insurance coverage. Although two independent arbitrators have already ruled on the Matter, the insurer was afforded this de novo review. Thus, in defending this action and seeking to establish that injuries were sustained, and no-fault benefits should be paid, the court held that the medical provider was entitled to comprehensive discovery to defend the action. The This included discovery of the nature of other arbitrations in which the insurer participated with other medical providers, what arguments were presented, what payments may have been made, what evidence was exchanged and how those arbitrations were resolved. The court held this information was highly relevant, material, and necessary, and therefore granted the motion seeking to have the insurer produce the entire file encompassing information regarding all other arbitrations concerning the insured.

The court also considered the insurer’s motion seeking a protective order and held that an order of confidentiality was appropriate pursuant to CPLR § 3103 to protect material confidential in nature, or information which is subject to abuse if widely disseminated. The court held there was no basis to deny the disclosure of the insurer’s claims file to the medical provider, the submission of a valid privilege log by the insurer presented sufficient evidence that a protective order should be granted to protect sensitive information from being disseminated to the public.

RYAN’S FEDERAL REPORTER

Ryan P. Maxwell

[email protected]

03/11/24 Liberty Mutual Insurance Company v. Day To Day Imports, Inc.

Southern District of New York

Insurer Successfully Combats Attempt to Depose Coverage Counsel Who Had Ghostwritten Reservations of Rights Letters

In a declaratory judgment action filed by Liberty Mutual Insurance Company against various parties following its issuance of reservations of rights letters, the defendants sought to “compel the deposition of William Fennell, an attorney formerly employed by Plaintiff's counsel.” This motion to compel was filed only after “an Order that . . . for the period from February 20, 2024, through March 10, 2024, fact discovery would be limited to [certain enumerated depositions not including Mr. Fennell]; and that additional discovery would be permitted only for extraordinarily good cause shown.” No mention of Mr. Fennell had been made to the court prior to this motion.

The SDNY found that Defendants “failed to demonstrate extraordinarily good cause to expand the remaining permissible scope of fact discovery to include the deposition of Fennell.” Although Defendants indicated that they did not advise the Court sooner because “they did not yet have the transcript from the claims handler's deposition, which led them to realize they needed Fennell's deposition, and because the parties had not yet met and conferred on the issue,” the attorneys had personal knowledge of the testimony without the transcript.

More interestingly from a practice pointer standpoint is Magistrate Judge Tarnofsky’s secondary conclusion, which begins that “I would not compel the Fennell deposition even if Defendants had told me at the February 1 conference that they were contemplating seeking this deposition.” Defendants had argued that Fennell “had ghostwritten two reservations of rights letters sent by Plaintiff to Defendants shortly after the fire that led to their insurance claims,” and that “as a result, Fennell engaged in claims-handling activity, which made his communications with Plaintiff discoverable.” However, Liberty correctly noted that “Fennell was not involved in Plaintiff's claims handling or claims adjustment process and that he “acted as coverage counsel” and not “as a claim investigator”; and that work product protection attaches to materials prepared after it decided to decline coverage in part before the letters were drafted.” The SDNY agreed with Liberty, finding that “Fennell acted as coverage counsel and did not engage in claims-handling activity,” such that Fennell's communications with Plaintiff are privileged, and so he may not be deposed by Defendants.”

The details relative to the issue of whether coverage counsel acted as claims handler are important. So, here they are:

Plaintiff's claims handler stated at his deposition that an attorney from the firm representing Plaintiff in connection with Defendants’ insurance claim drafted the two reservations of rights letters to Defendants but that he approved the letters. (Citation omitted). In Fennell's affirmation, he states that he “did not decid[e] whether the claim should be accepted and paid or rejected and denied” and that he prepared draft letters “based on information and facts provided by [Plaintiff] or its investigators, not any independent investigation.” (Citation omitted). This evidence supports a conclusion that Fennell acted as coverage counsel by performing analysis about coverage and making recommendations to Plaintiff, while Plaintiff's claims handler performed the investigation into the claim, provided information to Fennell, and made the ultimate decision on coverage. . . .

That Fennell's recommendations about coverage were contained in draft reservation of rights letters approved and adopted by Plaintiff and sent to Defendants does not, as Defendants suggest (Citation omitted), change the analysis. Defendants have the letters. They were entitled to ask the claims handler at his deposition about those letters and the basis for his decision to approve and send them, to the extent the questions did not invade the attorney-client privilege by asking about the legal advice provided by Fennell provided. But Defendants are not entitled to depose Fennell to ask about the legal advice he provided to the claims handler.

Maxwell’s Minute: The insurer was not attempting to “shield” discovery of relevant investigation. This was an insurer relying upon the guidance of coverage counsel following the insurer’s investigation of facts underlying a claim; a subtle distinction, but an important one.

If you would like a copy of the decision, which provides the legal backing for the Court’s conclusions, in addition to the above, please email me and I would be happy to provide it.

STORM’S SIU

Scott D. Storm

[email protected]

Flying back from vacation in Key West. Double the cases next edition.

FLEMING’S FINEST

Katherine A. Fleming

[email protected]

03/11/24 Gregory v. Safeco Ins. Co. of Am., Runkel v. Owners Ins. Co.

Colorado Supreme Court

Notice-Prejudice Rule Applies to Occurrence-Based First-Party Homeowners’ Property Insurance Claims

Gregory had a homeowners’ insurance policy with Safeco that contained a notice provision that notice must be within 365 days after the date of loss for loss caused by windstorm or hail. Gregory’s home was damaged by a hailstorm, but she claimed she did not become aware of the damage until eighteen months later. Safeco denied the claim, and Gregory filed suit in the District Court. The lower court granted Safeco’s motion for summary judgment. Gregory appealed, arguing that the district court had erred by not applying Colorado’s notice-prejudice rule to the notice-of-loss provision in her policy. The court of appeals affirmed, concluding that only the supreme court could extend the notice-prejudice rule to first-party claims under homeowners’ insurance policies. Instead, the court of appeals felt bound to apply the “traditional approach” under which the notice provision was a condition precedent to Gregory’s right to recover for the hail damage. Since she had not satisfied the condition precedent, the court of appeals determined that Gregory’s unexcused late notice relived Safeco of its obligation to cover the loss.

Similarly, the Runkels’ property sustained damage in a hailstorm, and they did not discover the damage until almost a year later. Owners denied the claim as untimely, and the Runkels sued. The district court granted Owners’ motion for summary judgment, concluding the notice-prejudice rule did not apply. The court of appeals cited Gregory and affirmed on appeal.

Gregory and the Runkels filed petitions for writs of certiorari, and the Colorado Supreme Court granted both. The Court considered whether the notice-prejudice rule, which allows an insurer to deny coverage based on a claim’s untimeliness if the insurer can show prejudice, applies to occurrence policies for first-party homeowners’ property insurance claims. The Court concluded that the notice-prejudice rule applies to occurrence-based, first-party homeowners’ property insurance policies. The Corut reasoned that recent case law has applied the notice-prejudice rule to occurrence policies like the one at issue in which the purpose of notice is to allow the insurer to investigate and defend against the claim and is not fundamental in defining the temporal boundaries of coverage. Further, the Court reasoned that the rule should apply because of the adhesive nature of insurance contracts, the public policy objective of compensating tort victims, and the inequality of granting the insure a windfall due to a technicality. Accordingly, the Court reversed and remanded.

GESTWICK’S GARDEN STATE GAZETTE

Evan D. Gestwick

[email protected]

On the road this edition. See you in two weeks.

O’SHEA RIDES the CIRCUITS

Ryan P. O’Shea

[email protected]

03/08/24 Meier v. Wadena Ins. Co

United States Court of Appeals, Seventh Circuit

Insured Cannot Avoid Appraisal Award Based on Argument that Lack of Policy Definition of Actual Cash Value Barred Application of Broad Evidence Rule

This case involved Ms. Meier submitting a first party property damage to Wadena under a commercial property insurance policy. Meier owned the Heartland Inn, a restaurant, that suffered extensive fire damage in June 2019. The Wadena policy entitled Meier to recover actual cash value (“ACV”) of the property, with a limit of approximately $1.1 million. However, the policy did not define ACV and the parties disagreed on how to calculate the ACV. Wadena paid Meier $775,000 and explained that is made payment pursuant to Wisconsin law by use of the “broad evidence rule,” which permits insurers to consider a variety of relevant evidence to determine the value of the property at the time of loss.

Displeased with Wadena’s payment, she sought the help of a third-party adjuster who estimated the ACV exceeded the policy’s limit. Wadena learned of the estimate and issued another check that brought Meier’s total recovery to $845,135.79. Still unsatisfied, Meier invoked her right to appraisal.

Meier sought appraisal under the policy, which the district court held her to. The district court found nothing wrong with that appraisal. The relevant appraisal provision, which is generally found in commercial property policies, provided:

“If we and you disagree on the amount of loss, either may make written demand for an appraisal of the loss. In this event, each party will select a competent and impartial appraiser. The two appraisers will select an umpire. If they cannot agree, either may request that selection be made by a judge of a court having jurisdiction. The appraisers will state separately the amount of loss. If they fail to agree, they will submit their differences to the umpire. A decision agreed to by any two will be binding.”

After the appraisal process began, Meier filed an action in the Eastern District of Wisconsin, which was dismissed due to Meier’s own choice to resolve the claim through appraisal, not litigation. That order required Meier to complete the appraisal. The appraisal process completed, and the independent umpire also used the “broad evidence rule” and looked to average market valuation, cost approach value, tax assessment, Wadena’s appraiser’s valuation, Meier’s appraiser’s repair estimate, and second repair estimate. The umpire determined the ACV was $939,136.58, Wadena’s appraiser agreed to the estimate, therefore, making the appraisal binding. Wadena increased its payment to meet the appraisal award.

Meier then filed a second suit in state court suit naming Wadena and the umpire as defendants for breach of contract, bad faith, and sought to set aside the appraisal award as invalid under Wisconsin state law. The state court dismissed the umpire, whereafter Wadena removed to federal court based upon diversity jurisdiction. Wadena moved to dismiss based upon Meier’s election to proceed with appraisal. The district court agreed and dismissed Meier’s second suit finding Wadena acted in accordance with the policy provision and nothing in Wisconsin law nor the policy barred the use of the broad evidence rule. Meier then appealed and Wadena cross-appealed for denial of its request for sanctions.

The Seventh Circuit found, where a party elects appraisal in an insurance policy, Wisconsin law backs that choice. Specifically, that parties in an appraisal agree to remove a jury and judge from interfering from that decision. Generally, Wisconsin courts treat appraisal awards as presumptively valid and may only be set aside upon the showing of fraud, bad faith, a material mistake, or a lack of understanding or completion of the contractually assigned task. On the last method to set aside an appraisal award, Wisconsin case law notes that the court’s role is not to determine whether an accurate valuation occurred or whether the court could do a better job, but whether the third-party experts understood and carried out the contractually assigned task.

The court rejected Meier’s argument that the umpire did not understand the task because the broad evidence rule was not permitted in the policy due to ACV being undefined. The court cited two Wisconsin Supreme Court decisions that explained insurers may use the broad evidence rule to calculate ACV when the policy does not define the term. The court further rejected Meier’s argument that sought a nuanced application of Wisconsin insurance law to prohibit the use of the broad evidence rule. The court did so by noting the authority relied upon by Meier held that appraisers are to us a logical, predictable approach rather than a free for all when applying the broad evidence rule; and that it did not prohibit the rule’s use. Due to Wadena’s agreement and payment of the appraisal award, the Seventh Circuit found Wadena complied with the appraisal provision.

By determining Wadena’s compliance with policy, the court dismissed Meier’s breach of contract and bad faith claims. As for the sanctions, the court affirmed the district court’s decision. It found that while Meier’s argument was a long shot, it was not a frivolous claim requiring sanctions.

03/07/24 Amerisure Ins. Co. v. Auchter Co.

United States Court of Appeals, Eleventh Circuit

Resolution of Issue Did Not Judicially Resolve Crossclaim Barring Court from Hearing Appeal Due to Lack of Final Judgment

Riverside owned a property in Jacksonville, Florida and hired Autcher to build a 13-story office building. The project was plagued by delays and water intrusion, which culminated in Riverside filing a state suit in Florida seeking a declaratory judgment establishing Authcer’s (and Arch Insurance Company, Autcher’s surety) for breach of contract and performance bond. Arch filed a counterclaim against Riverside seeking payment of the construction contract balance, for approved change orders, as well as for payments of disputed charges and delay damages.

Autcher and Arch also filed a third-party action against TSG, the window subcontractor, and other subcontractors for contractual indemnity and breach of contract alleging that Riverside’s claims implicated the scope of work on each respective subcontract. Landmark, TSG’s insured, acknowledged Autcher as an additional insured but denied Autcher a defense. Due to this, Amerisure, Autcher’s primary insurer, defended Autcher under a reservation of rights.

After trial, the state court entered judgment (1) in favor of Riverside against Arch and Autcher; (2) in favor of Arch against TSG; and (3) in favor of Autcher and Arch against B&B, the subcontractor for curbs, storm drainage, and landscaping. After the state court judgment, Amerisure filed the present action against Landmark, Autcher, Arch, Riverside, TSG, and B&B seeking a declaration that it owed no duty to indemnify Autcher and Arch, and demanding reimbursement from Landmark for the cost of defending Auchter.

Several crossclaims ensued, which included one by Landmark against TSG that Landmark had no duty to defend nor indemnify TSG for the state court action. Years later after many summary judgments, as well as a settlement between Arch and Amerisure, the district court granted Amerisure’s entry for final judgment against Landmark only, finding that Amerisure was entitled to attorney’s fees and cost. This appealed followed.

The question presented is whether the district’s court decision actually constituted a “final judgment”. The court noted that a final judgment is one that resolves the merits and leaves nothing for the court to do but execute the judgment and that a decision adjudicating something less than adjudication of all claims is not a final judgment. The court further explained an exception to this rule is where a district court certifies a judgment as final under Fed. R. Civ. P 54(b).

Amerisure’s argument in post-argument briefing was that the underlying declaratory judgments resolved the issues of Landmark’s obligations to indemnify other parties, including TSG. The court found even if the issue of Landmark’s duty to indemnify other parties has been effectively answered, the crossclaim itself was still not answered. The court reasoned that resolution of abstract issues did not resolve the tangible claim. Based upon the finding that Landmark’s tangible crossclaim was unresolved, the Eleventh Circuit found lack of jurisdiction to hear the appeal.

LOUTTIT’S LEGISLATIVE and REGULATORY ROUNDUP

Robert P. Louttit

[email protected]

Nothing to report at this time.

ROB REACHES the THRESHOLD

Robert J. Caggiano

[email protected]

02/20/24 Perez v. Ahadzi

Appellate Division, First Department

First Department Unanimously Affirmed, Without Costs, a Decision Granting Summary Judgment in Favor of Defendant Where Plaintiff’s Evidence Failed to Raise an Issue of Fact on Whether He Suffered Serious Injury Within the Meaning of Insurance Law § 5102(d).

Plaintiff appealed from an Order of Supreme Court, New York County, which granted Defendant’s motion for summary judgment dismissing the complaint on the ground that Plaintiff did not sustain a serious injury within the meaning of Insurance Law § 5102(d). On review, the First Department unanimously affirmed granting of the motion, finding the evidence presented in opposition failed to raise an issue of fact.

By way of background, this matter stems from a motor vehicle accident, where a vehicle owned and operated by Defendant, Gladstone Ahadzi, struck the vehicle owned and operated by Plaintiff Ruben Perez. As a result of the collision, Plaintiff asserted significant and permanent injuries to his left wrist, left shoulder, cervical spine, and thoracic spine. Notably, in motion practice Plaintiff also alleged a lumbar spine injury – but the Supreme Court was not required to consider such injury claim as Plaintiff failed to allege it in either his complaint or bill of particulars.

On review, the First Department started its analysis by confirming the lower court’s finding that the Defendant met its initial burden for summary judgment dismissing the complaint. Specifically, Defendant relied upon a radiologist report which opined that positive findings on Plaintiff’s spinal MRIs were chronic, degenerative, and preexisting, and therefore not related to the accident. Further, the radiologist opined that an MRI of Plaintiff’s left shoulder was unremarkable. Defendant also produced a report of an IME orthopedic surgeon who examined the plaintiff and found him to have normal range of motion and no positive exam findings.

In opposition, the First Department also confirmed the lower court’s finding that Plaintiff failed to raise a triable issue of fact. First, it was highlighted that most of Plaintiff’s opposition consisted of unaffirmed medical records. Specifically, the opinion submitted by plaintiff’s physician opining permanency was found to be speculative, as there was a three-and-a-half-year gap between dates when the physician examined the Plaintiff. Further, it was noted that Plaintiff’s prompt return to his job as a doorman after the accident and minimal treatment for about six months post-accident, demonstrate that any injury sustained was minor in nature. Lastly, the First Department dismissed any claim for the 90/180 category of § 5102(d), as there was no evidence showing a causal nexus between the accident and injury.

Accordingly, the First Department unanimously affirmed the Supreme Court, New York County’s, Decision granting summary judgment in favor of the Defendant dismissing the complaint against it, without costs.

GOLDBERG’S GOLDEN NUGGETS

Joshua M. Goldberg

[email protected]

03/13/24 Kerper v Betancourt

Appellate Division, Second Department

Defendant Rear Ended by Plaintiff Loses Motion for Summary Judgment

In this rear-end motor vehicle accident, Defendant’s vehicle was stopped at the time his vehicle was struck in the rear by Plaintiff. Defendant testified that he had come to a gradual stop with his left turning signal on, waiting for traffic to clear before making his turn. Based on this testimony and the certified police accident report, Defendant’s motion for Summary Judgment was granted by the trial court. However, on appeal, the Appellate Division found that Plaintiff raised a triable issue of fact by raising credibility issues as to whether Defendant came to a gradual stop, instead of a sudden stop, and whether Defendant utilized his turning signal.

03/14/24 Matter of Mina v New York City Tr. Auth.

Appellate Division, Third Department

Reasonableness of IME Location

In this appeal out of the Workers’ Compensation Board, the claimant contends that a Manhattan IME location scheduled 22.3 miles away from his New Jersey residence was unreasonable and his non-appearances were based upon good cause. The Administrative Law Judge, affirmed by the Workers’ Compensation Board on administrative appeal, found that the Claimant failed to establish good cause for his non-appearances, but directed that the Employer schedule an IME within 30 miles of the Claimant’s home in New Jersey.

On appeal, the Third Department affirmed the decision of the Workers’ Compensation Board. Interpreting WCL §137[4], which provides, as relevant, "[a]ll independent medical examinations shall be performed in medical facilities suitable for such exam, with due regard and respect for the privacy and dignity of the injured worker as well as the access and safety of the claimant. Such facilities must be provided in a convenient and accessible location within a reasonable distance from the claimant's residence." In upholding the determination that the location of the IME was not unreasonable, the Appellate Division pointed to the fact that the Claimant is driven by his daughter to his treating physicians in Brooklyn, 39 miles away, was substantial evidence that supported the Workers’ Compensation Board determination.

Note: While this case arises from the Workers’ Compensation Board, it provides a rare and valuable analysis of the reasonableness of a designated IME location as viewed in other contexts, such as No-Fault, UM/UIM disputes, and other personal injury actions.

LABARBERA’S LOWER COURT LIBRARY

Isabelle H. LaBarbera

[email protected]

02/27/24 Bronstein Props. LLC v. Wesco Ins. Co.

Supreme Court of the State of New York, New York County

Insured’s Declaratory Judgment Action Dismissed On Summary Judgment Pursuant to the Suit Limitation Clause in Policy

Bronstein Properties LLC and Heights 178 LLC filed a declaratory judgment action seeking a determination that their commercial property insurer was required to provide coverage for loss at the insured property.

The loss stemmed from cracking walls at the property. After the New York City Department of Buildings issued a violation on the property, the insured reported the loss to their insurer on July 14, 2016. However, during the investigation it was revealed that the plaintiffs had previously hired an engineer, who had been inspecting cracks in the building as far back as August 2014. On May 31, 2018, the insurer disclaimed coverage for the damage. The insurer determined that the damage fell under four separate policy exclusions, including normal settling, earth movement, structural impairment, and faulty workmanship. Additionally, the insurer asserted that there was a violation of the notice provision in the policy.

The policy’s notice provision required the insured to give the insurer prompt notice of any loss or damage. Additionally, the policy contained a suit limitation provision, which stated that any lawsuit made against the insurer must be made within two years after the date on which the direct physical loss or damage occurred.

The insurer made a motion for summary judgment, seeking dismissal of the complaint. The insurer argued there was no coverage under the subject policy because of the breach of the notice condition, the breach of the suit limitation provision, and the applicability of the policy’s exclusions. The court began their analysis with a recitation of the standard for review on a motion for summary judgment.